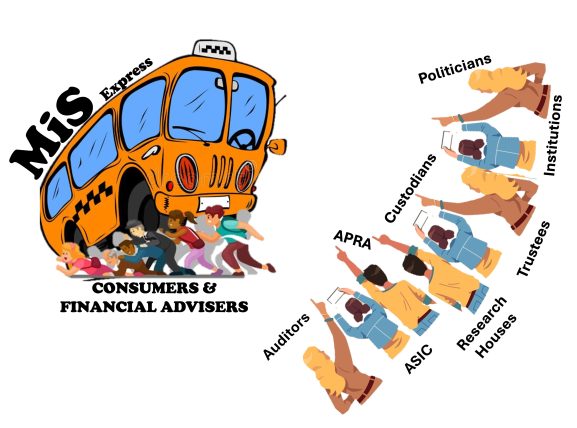

AIOFP says banks should stay out of advice ‘of any description’

The AIOFP has penned an open letter to Michelle Levy.

The Association of Independently Owned Financial Professionals (AIOFP) has addressed an open letter to Quality of Advice Review (QAR) lead Michelle Levy arguing against the return of banks to financial advice.

To underpin its argument that banks should remain at arm’s length, the AIOFP attached a list of 191 product failures to its letter.

“Attached is clear evidence of how the banks/institutions have managed their products since 2006 and specifically incorporating the GFC crisis,” said AIOFP executive director, Peter Johnston.

“Their management skills have been woeful; the funds have generally performed poorly with capital losses and expensive compared to other options like the Industry Superannuation funds sector. As you will see, there are 191 funds with $43 billion of consumers capital either failed, frozen or impaired,” he continued.

According to Mr Johnston, the banks should stay out of advice “of any description” and stick to what they do best — “standard banking, administration, management activities”.

“In fact, when you consider how poorly the banks have performed in the wealth space over the years with inflicting consumer capital losses, no advice will be better than getting advice from them for most consumers,” the executive director said.

“We hastened to add that the advice community has been inexplicably blamed for these failures

whilst the institutions and regulators run for legal cover. As you no doubt know, advisers just recommend them, ASIC register them, banks/custodians/trustees manage them and research houses rate them,” Mr Johnston opined.

“Considering the world is likely to be entering into another GFC similar event in 2023, we would suggest consumers are better to leave their cash in a savings account rather than running to the banks looking for solutions.”

His solution to the compliance burden imposed on advisers is a truce between ASIC and representatives of the advice industry in the form of an afternoon meeting.

“The perennially discussed ridiculous levels of unnecessary compliance loaded onto advisers and consumers over the past seven years could be resolved in an afternoon between ASIC and representatives of the advice industry,” Mr Johnston said.

“This should reduce the cost of advice by at least 50 per cent and even further if other options are implemented”.

Last week, the lead of the Quality of Advice Review argued that “advice is episodic” and “so we need a diversity of providers and the obvious candidates are the people that look after our money or lend us money.”

Ms Levy said she wants “to encourage banks and other institutions to use the information they have to advise their customers”.

Her words, spoken at The AFR Super and Wealth Summit, sparked an impassioned reply from ifa’s readership, with many questioning the merits of the QAR and the outcomes it could yield.